{kind=link}

What’s the influence of being insured on well being outcomes? This can be a troublesome query to reply partially due to hostile choice (e.g., sicker sufferers might select to be insured). However even absent hostile choice, the flexibility to analysis a illness might range between the insurer and uninsured. Think about this instance from Kaliski (2023):

For instance, higher entry to testing improves the speed at which SARS-COV2 infections are detected. If we naively in contrast the dying fee from these infections amongst insured people to that amongst uninsured people, we will likely be overestimating the impact of entry to insurance coverage. This will likely be as a result of uninsured people can have fewer detected circumstances of SARS-COV2, artificially shrinking the denominator when dividing the variety of deaths by the variety of circumstances.

The paper goes on assist sure any biases as a consequence of differential charges of analysis between the insured and uninsured. The authors use a monotonicity assumptions much like the one utilized in Manski and Pepper (2000), so long as the route of any choice bias is understood. The 2 key monotonicity assumptions are:

- Monotone Subgroup Choice. On this context, it implies that any given particular person is at all times at the least as prone to be recognized with a illness if they’d insurance coverage in comparison with if they didn’t have insurance coverage. Very believable.

- Monotone Analysis Response. This assumption implies that any particular person recognized with the illness have at the least nearly as good outcomes as those that are undiagnosed. That is true so long as physicians should not actively harming sufferers as soon as recognized…once more, very believable.

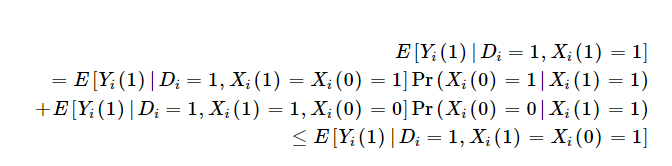

One implication is that those that are influence of insurance coverage on outcomes is the weighted sum of the influence of insurance coverage on outcomes amongst those that would at all times be recognized with or with out insurance coverage [Xi(1)=Xi(0)=1] and people would solely be recognized with insurance coverage [Xi(1)=1; Xi(0)=0]. As a result of insurance coverage might result in therapy in addition to enhance the chance you might be recognized, the profit among the many insured is weakly bounded by outcomes amongst insured people who would solely be recognized if they’ve insurance coverage. That is described mathematically utilizing the Monotone Analysis Response assumption under as:

Furthermore, if we mix this with the Monotone Subgroup Choice assumption, Kaliski exhibits that the “diagnosis-constant” subgroup-specific impact of therapy on the handled is at the least as giant because the pattern estimate of the subgroup-specific therapy impact.

Kaliski additionally notes that if there the information being analyzed has a proxy for common outcomes among the many undiagnosed within the management group (i.e., no insurance coverage), however obtain a analysis within the handled group, then one can determine the diagnosis-constant therapy impact with the belief that both:

- (i) those that could be within the subgroup of curiosity no matter publicity to therapy, or

- (ii) the newly recognized, when uncovered to the therapy that causes their new analysis, should not chosen for idiosyncratic time traits.

Mathematically that is:

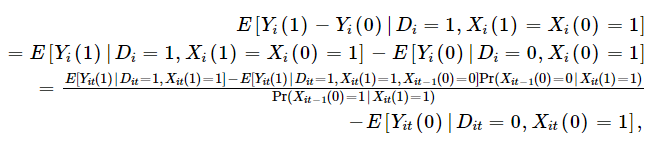

One can then mainly, use the chance recognized individuals with insurance coverage weren’t recognized earlier than they’d insurance coverage to regulate the noticed outcomes among the many insured. This software requires panel information, however if in case you have panel information, one can calculate as follows:

Kaliski, then applies this technique to look at the influence of insurance coverage protection for insulin therapy for diabetes on outcomes. The exogenous change in chance of insurance coverage is–unsurprisingly–the transition to Medicare when individuals flip 65. Kaliski makes use of HRS information, which has a panel construction and permits one to look at how analysis charges modifications earlier than and after transitioning to Medicare both from industrial/Medicaid/different insurance coverage or from no insurance coverage. Utilizing this strategy, he finds that:

Utilizing a regular difference-in-discontinuities estimator, and ignoring the impact of recent diagnoses, I discover a 3% level enhance in initiation of insulin use amongst people with diabetes once they flip 65 in 2006–2009 relative to those that flip 65 in 1998–2005. Accounting for the rise in diagnoses of diabetes that happens at age 65 in 2006–2009 (Geruso & Layton, 2020), I discover that the true impact amongst those that already had been recognized earlier than age 65 is prone to be at the least as giant as the purpose estimate; exploiting panel information to determine the speed of initiation among the many newly recognized at age 65, I discover that the true impact is 0.6% factors bigger, 20% bigger in relative phrases.

Briefly, simply evaluating insulin use amongst insured vs. non-insured was 3%, however in actuality the true quantity ought to have been 3.6% as a result of not solely did Medicare insurance coverage result in extra individuals who have been already recognized getting therapy, but in addition extra individuals have been recognized with diabetes and thus acquired therapy.

The complete paper may be learn right here.